George Rebane

As investment guru Porter Stansberrry (Stansberry & Associates) reviews the Obama onslaught with historical levels of printing money, raising taxes, and legislating new productivity killing laws into place, he summarizes with –

… these fears ought to apply equally to Democrats or Republicans. If you were trying to devise a political plan to destroy the country, this is the route you’d take: make it harder than ever before to produce anything, devalue the currency, and raise taxes by 50%.

And for those who are betting on the recent “glimmer” in Obama’s eye, financial academic and blogger Adam Levitin of Credit Slips reminds us of the mortgage reset tsunami still heading for us.

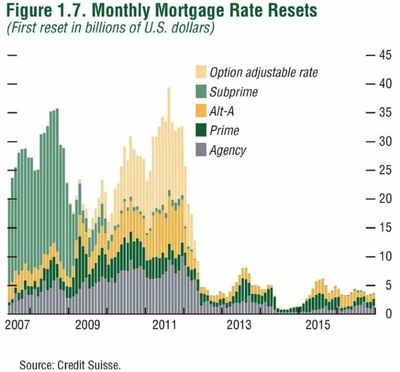

… it’s worth remembering that only 14% of mortgages outstanding are subprime. Most mortgages aren’t subprime. To be sure, a disaster in 14% of the market is a huge problem in and of itself. But this graph from Credit Suisse is the most sobering thing I’ve seen in a while. It shows that most of the interest rate resets ahead aren’t subprime, but are instead Alt-A and option-ARMs. Alt-A is the category of loans made to consumers with FICO scores just above the subprime threshold. Option ARMs give borrowers several payment options, including making a minimum payment that does not even cover the interest that accrued in the last month. This means it’s pretty easy for an option ARM to end up underwater, even in a market where prices are holding steady. If real estate prices are dropping, it is even more likely that an option ARM will end up upside down, which makes refinancing near impossible. The bulk of the Alt-A and option-ARM resets are coming in 2010-2011. A lot of things could change before then. But we might just be seeing the tip of the iceberg in the housing market.

And from the graph you can see that here in 2009 we are in the relatively calm eye of the storm.

Leave a comment