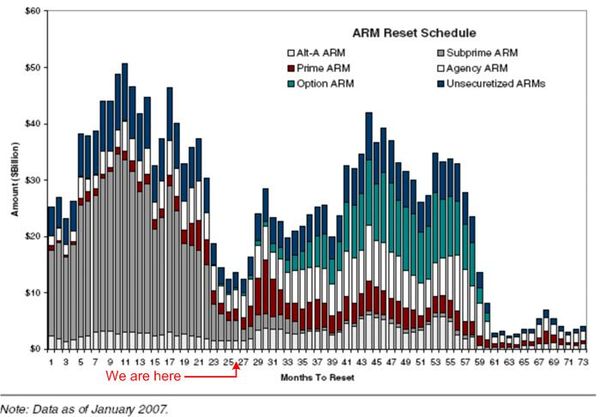

[This piece was submitted by John ‘Red’ Burke, branch manager of the Grass Valley office of First Priority Financial – formerly Burke Home Loans. John is a long time real estate finance professional who follows closely what is happening in this keystone sector of the national economy. I have included a figure showing the magnitude of the adjustable rate mortgage reset schedule since January 2007. gjr]

John ‘Red’ Burke

This is an economics and mortgage market analysis for the January period. Some of my take-aways are:

1) The general public doesn’t appreciate how close we came to a complete financial meltdown:

The Fed stepped up immediately and averted what could well have been the depression scenario that many feared. Had short-term corporate borrowing remained frozen, there would have been the potential for massive job losses as payroll funding would have been unavailable.

2) The employment market is UGLY:

Weekly unemployment claims are averaging around 550,000, the highest level since the early 1980s.

3) Consumers are hunkering DOWN:

Consumers have established a solid trend line of declining credit demand with credit balances falling for three of the last four months. This has been evident as the end-of-year retail sales data were the worst since 1970 (using chain store sales). If this shift is a sign that consumers really are transitioning from a mindset of consumption based on access to credit to a mindset of savings and consumption balance, then the recovery of the economy is likely to be slow irrespective of any stimulus. The bleeting masses, when forced understand how to balance a budget (unlike our legislators).

4) Buyers have to actually QUALIFY for their loans using government tax documents. This is bad news for the Self-Employed and Under-the-Table people who were gaming the tax system. I would estimate that historically 50% of our Nevada County clients needed to state income to qualify for a loan. Typically, our analysis of their income coming into their business & personal checking accounts validated their capacity to debt service a mortgage payment despite what their tax returns showed.

The homeownership rate has also been coming down and there has been some argument that by lowering mortgage rates to 4.5 percent enough new borrowers can be brought into the market to return the homeownership rate back to its peak of over 69 percent. However, that assumes that the credit and house price bubbles did not artificially inflate the homeownership rate. In fact, our internal calculations indicate that the actual number of new homeowners created by the rate decline will be very small.

5) We have not seen the peak or halfway point of the homes that will be foreclosed on. The Lenders stopped/froze the foreclosure process in early November. Lenders didn’t want the bad press of evicting families from their homes over the Holidays (Thanksgiving, Christmas, New Years, etc.). Internal memos from the Lenders to their REO Realtors are advising them to ramp-up their operations and staff for the coming tsunami of REO properties.

The big problem continues to be inventory, and the inventory of total homes on the market is still near the peak as foreclosures come close to replacing sales. That said, the inventory is down from its absolute peak and to the extent that the lower expected mortgage rates occur and remain there, the incremental addition of owners will help.

6) FannieMae and FreddieMac are actually impeding the housing recovery. They are insisting on receiving “delivery fees” of 0.50 point ($500 per $100,000) on every loan. FreddieMac just bumped their “delivery fee” to 1.00 point ($1,000). Raising fees (ie. buyer costs) won’t help us work through this crisis.

One frustration, however, has been the stubborn spread between the 30-year fixed-rate market interest rate and the conventional conforming secondary market yield on Fannie Mae securities. This spread traditionally reflected the servicing fee and guaranty fee averaging 40 to 50 basis points over time. It remains in the range of 100 basis points currently. Thus, while market rates have come down, a return to historical averages for the secondary market spread would bring them down another significant amount.

7) We will NOT see a refi boom that exceeds previous refi cycles. Extensive restrictions have been put in place to eliminate the potential of loan defaults. These restrictions will throttle the recovery and will push marginal but viable borrowers “off the cliff”.

While at first glance this information would lead one to believe that we will see the largest refinance boom ever recorded, declining home prices, tighter credit conditions, and a bifurcation of the mortgage market into conforming and jumbo loans should dampen demand for refinancing.

Leave a comment